Bayesian Estimation of DSGE Models with Hamiltonian Monte Carlo

Bimodality in SW07 model - SHMC

Bimodality in SW07 model - SHMCAbstract

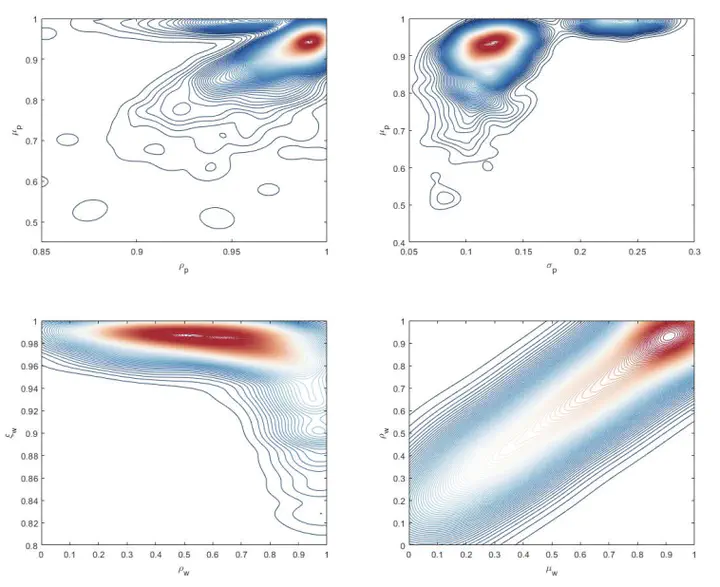

In this paper we adapt the Hamiltonian Monte Carlo (HMC) estimator to DSGE models, a method presently applied in various fields due to its superior sampling and diagnostic properties. We implement it into a state-of-the-art, freely available high-performance software package, Stan. We estimate a small scale textbook New-Keynesian model and the Smets-Wouters model using US data. Our results and sampling diagnostics confirm the parameter estimates available in existing literature. In addition, we find bimodality in the Smets Wouters model even if we estimate the model using the original tight priors. Finally, we combine the HMC framework with the Sequential Monte Carlo (SMC) algorithm to create a powerful tool which permits the estimation of DSGE models with ill-behaved posterior densities.